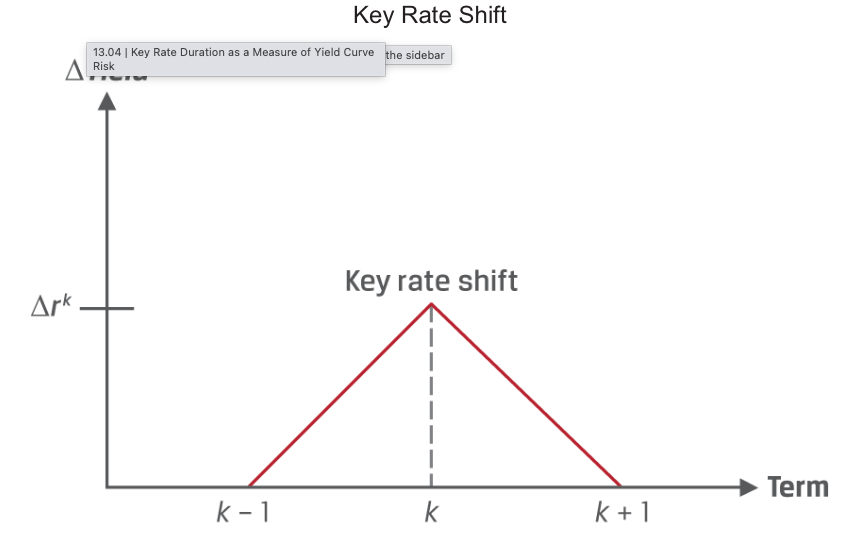

Key rate duration (or partial duration) is a measure of a bond’s sensitivity to a change in the benchmark yield at a specific maturity. Such a measure is important to isolate the price responses of bonds to changes in the rates of key maturities on the benchmark yield curve.

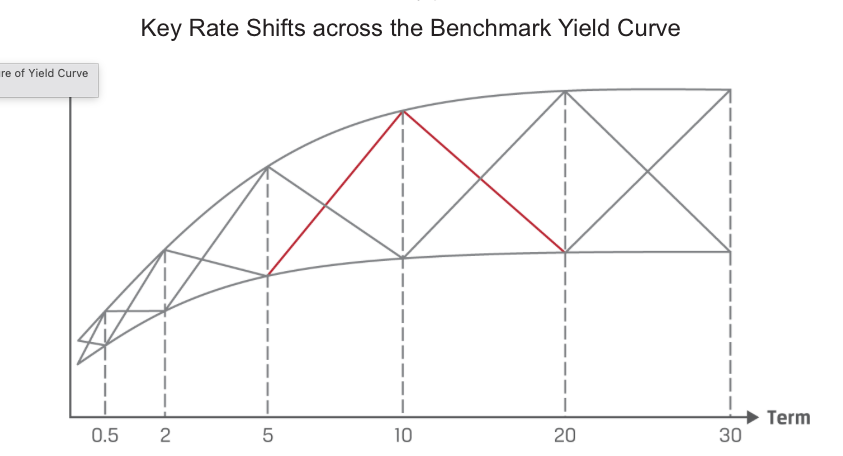

Key rate durations define a security’s price sensitivity over a set of maturities along the yield curve, with the sum of key rate durations being equal to the effective duration,