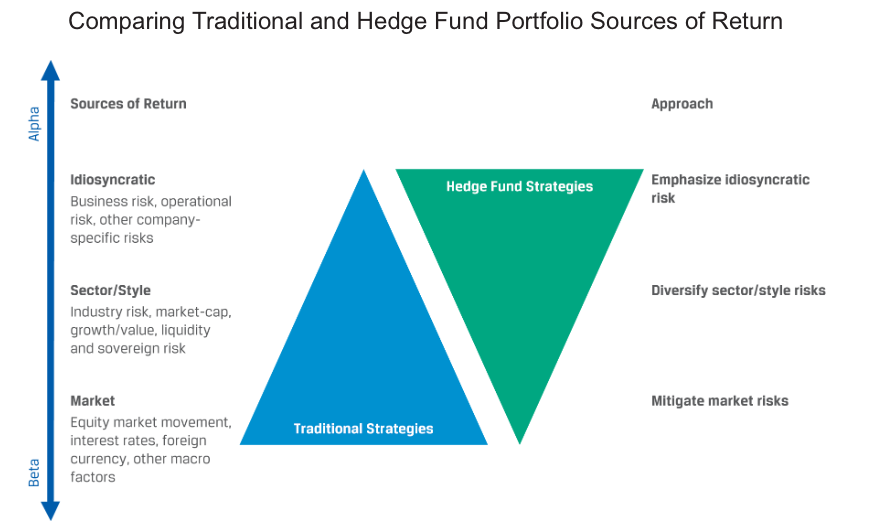

Some specific sources of alpha are the manager skills in specific stock selection and utilising higher-return strategies that minimise risks. The performance of hedge funds can be attributed to three distinct sources:

- Market beta—the broad market beta that can be realised using market index–based funds/ETFs

- Strategy beta—the beta attributed to the investment strategy of the hedge fund applied across the broad market

- Alpha—the manager-specific returns, due to the selection of specific positions

Hedge Fund Investment Risks and Returns