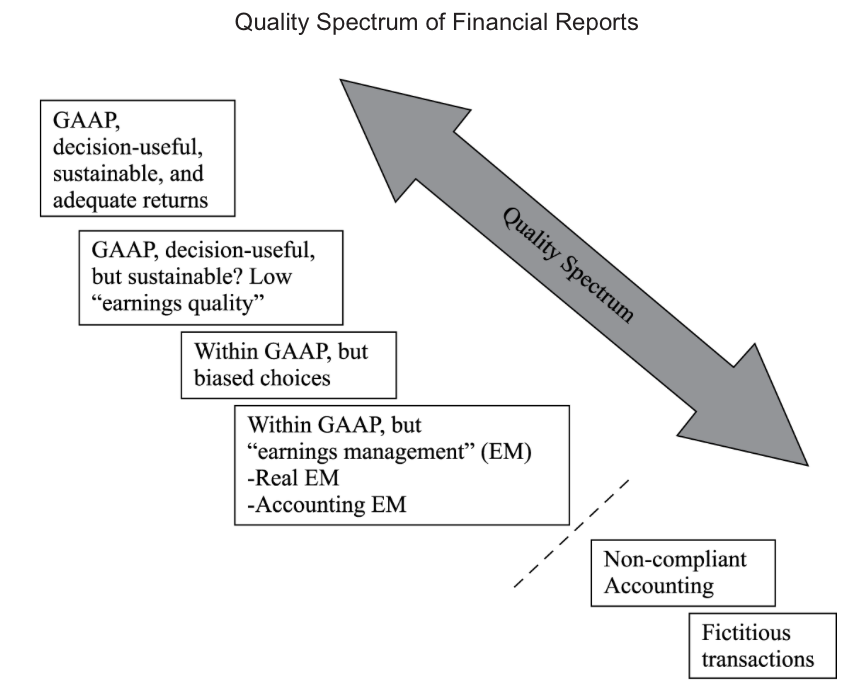

Ideally, analysts would always have access to financial reports that are based on sound financial reporting standards, such as those from the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB), and that are free from manipulation. But, in practice, the quality of financial reports can vary greatly. High-quality financial reporting provides information that is useful to analysts in assessing a company’s performance and prospects. Low-quality financial reporting contains inaccurate, misleading, or incomplete information.

Financial reporting quality pertains to the quality of information in financial reports, including disclosures in notes. High-quality reporting provides decision-useful information, which is relevant and faithfully represents the economic reality of the company’s activities during the reporting period as well as the company’s financial condition at the end of the period. A separate but interrelated attribute of quality is quality of reported results or earnings quality, which pertains to the earnings and cash generated by the company’s actual economic activities and the resulting financial condition. The term “earnings quality” is commonly used in practice and will be used broadly to encompass the quality of earnings, cash flow, or balance sheet items. High-quality earnings result from activities that a company likely will be able to sustain in the future and provide a sufficient return on the company’s investment. The concepts of earnings quality and financial reporting quality are interrelated because a correct assessment of earnings quality is possible only when there is some basic level of financial reporting quality. Beyond this basic level, as the quality of reporting increases, the ability of financial statement users to correctly assess earnings quality and to develop expectations for future performance also increases.