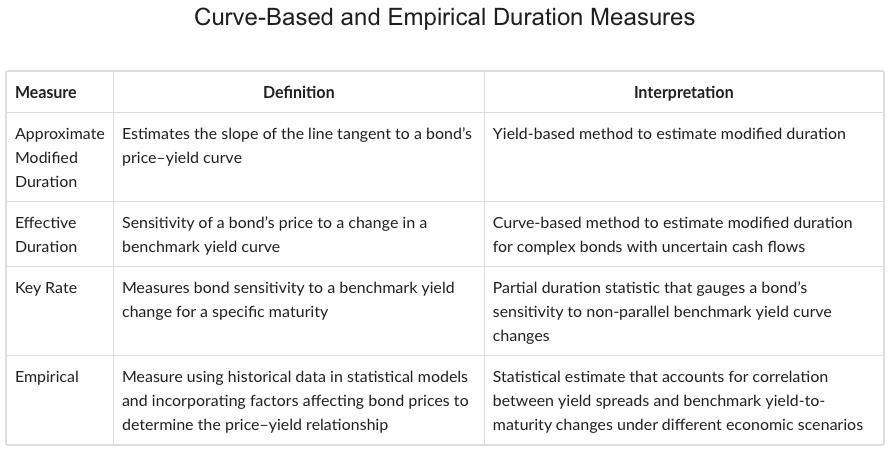

The approaches taken so far to estimate duration and convexity statistics using mathematical formulas is often referred to as analytical duration; the measures we have covered are summarised as follows:

In practice, there is another important type of duration: Fixed-income professionals often use historical data in statistical models that incorporate various factors affecting bond prices to calculate empirical duration estimates.