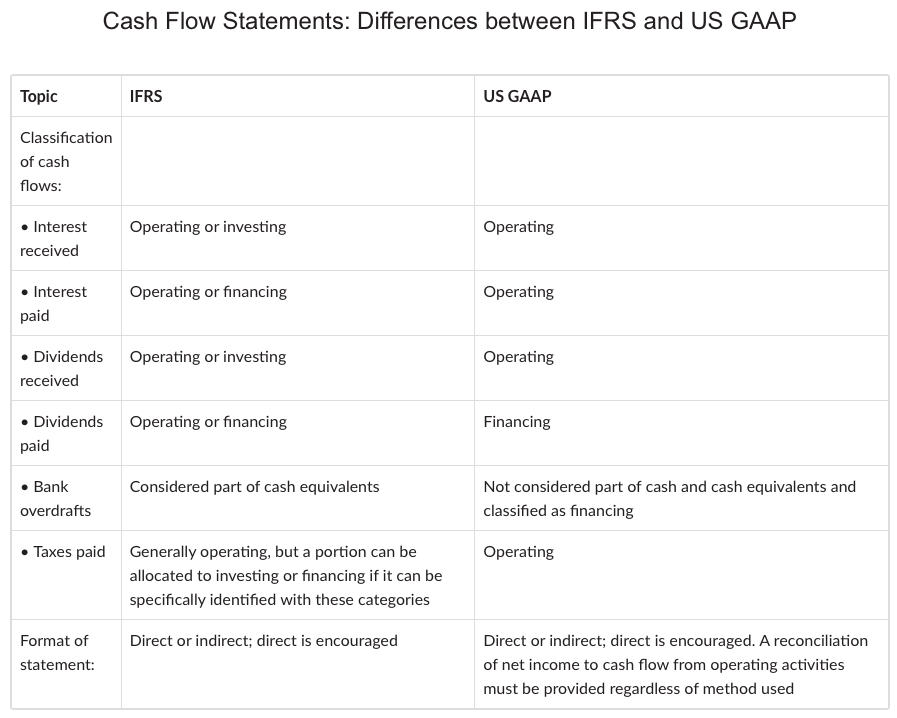

Most significantly, IFRS allow more flexibility in the reporting of such items as interest paid or received and dividends paid or received and in how income tax expense is classified.

US GAAP classify interest and dividends received from investments as operating activities, whereas IFRS allow companies to classify those items as either operating or investing cash flows. Likewise, US GAAP classify interest expense as an operating activity, even though the principal amount of the debt issued is classified as a financing activity. IFRS allow companies to classify interest expense as either an operating activity or a financing activity. US GAAP classify dividends paid to stockholders as a financing activity, whereas IFRS allow companies to classify dividends paid as either an operating activity or a financing activity.

US GAAP classify all income tax expenses as an operating activity. IFRS also classify income tax expense as an operating activity, unless the tax expense can be specifically identified with an investing or financing activity (e.g., the tax effect of the sale of a discontinued operation could be classified under investing activities).